CPA-REGULATION Online Practice Questions and Answers

In evaluating the hierarchy of authority in tax law, which of the following carries the greatest authoritative value for tax planning of transactions?

A. Internal Revenue Code.

B. IRS regulations.

C. Tax court decisions.

D. IRS agents' reports.

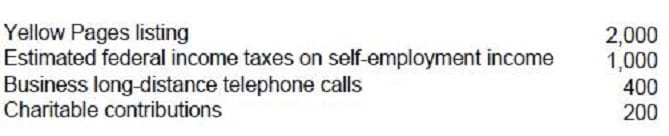

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich's cash disbursements were as follows:

What amount should Rich report as net self-employment income?

A. $15,100

B. $14,900 C. $14,100

D. $13,900

On February 1, 1993, Hall learned that he was bequeathed 500 shares of common stock under his father's will. Hall's father had paid $2,500 for the stock in 1990. Fair market value of the stock on February 1, 1993, the date of his father's death, was $4,000 and had increased to $5,500 six months later. The executor of the estate elected the alternate valuation date for estate tax purposes. Hall sold the stock for $4,500 on June 1, 1993, the date that the executor distributed the stock to him. How much income should Hall include in his 1993 individual income tax return for the inheritance of the 500 shares of stock, which he received from his father's estate?

A. $5,500

B. $4,000

C. $2,500 D. $0

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000

B. $59,000

C. $62,000

D. $84,000

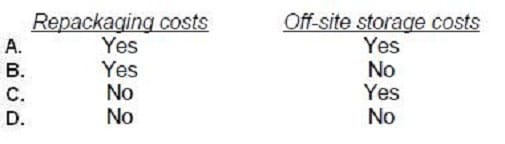

Under the uniform capitalization rules applicable to taxpayers with property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions have been met?

A. Option A

B. Option B

C. Option C

D. Option D

Smith made a gift of property to Thompson. Smith's basis in the property was $1,200. The fair market value at the time of the gift was $1,400. Thompson sold the property for $2,500. What was the amount of Thompson's gain on the disposition?

A. $0

B. $1,100

C. $1,300

D. $2,500

Greller owns 100 shares of Arden Corp., a publicly-traded company, which Greller purchased on January 1, 2001, for $10,000. On January 1, 2003, Arden declared a 2-for-1 stock split when the fair market value (FMV) of the stock was $120 per share. Immediately following the split, the FMV of Arden stock was $62 per share. On February 1, 2003, Greller had his broker specifically sell the 100 shares of Arden stock received in the split when the FMV of the stock was $65 per share. What is the basis of the 100 shares of Arden sold?

A. $5,000

B. $6,000

C. $6,200

D. $6,500

Clark bought Series EE U.S. Savings Bonds after 1989. Redemption proceeds will be used for payment of college tuition for Clark's dependent child. One of the conditions that must be met for tax exemption of accumulated interest on these bonds is that the:

A. Purchaser of the bonds must be the sole owner of the bonds (or joint owner with his or her spouse).

B. Bonds must be bought by a parent (or both parents) and put in the name of the dependent child.

C. Bonds must be bought by the owner of the bonds before the owner reaches the age of 24.

D. Bonds must be transferred to the college for redemption by the college rather than by the owner of the bonds.

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040. In 1992, Joan received an acre of land as an inter-vivos gift from her grandfather. At the time of the gift, the land had a fair market value of $50,000. The grandfather's adjusted basis was $60,000. Joan sold the land in 1994 to an unrelated third party for $56,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

K. $10,000

L. $25,000

M. $50,000

N. $55,000

O. $75,000

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040. Tom's 1994 wages were $53,000. In addition, Tom's employer provided group-term life insurance on Tom's life in excess of $50,000. The value of such excess coverage was $2,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

K. $10,000

L. $25,000

M. $50,000

N. $55,000

O. $75,000