CPA-TEST Online Practice Questions and Answers

In the first audit of a client, an auditor was not able to gather sufficient evidence about the consistent application of accounting principles between the current and prior year, as well as the amounts of assets or liabilities at the beginning of the current year. This was due to the client's record retention policies. If the amounts in question could materially affect current operating results, the auditor would:

A. Be unable to express an opinion on the current year's results of operations and cash flows.

B. Express a qualified opinion on the financial statements because of a client-imposed scope limitation.

C. Withdraw from the engagement and refuse to be associated with the financial statements.

D. Specifically state that the financial statements are not comparable to the prior year due to an uncertainty.

Which of the following is a conceptual difference between the attestation standards and generally accepted auditing standards?

A. The attestation standards provide a framework for the attest function beyond historical financial statements.

B. The requirement that the practitioner be independent in mental attitude is omitted from the attestation standards.

C. The attestation standards do not permit an attest engagement to be part of a business acquisition study or a feasibility study.

D. None of the standards of fieldwork in generally accepted auditing standards are included in the attestation standards.

Which of the following tests of controls most likely would help assure an auditor that goods shipped are properly billed?

A. Scan the sales journal for sequential and unusual entries.

B. Examine shipping documents for matching sales invoices.

C. Compare the accounts receivable ledger to daily sales summaries.

D. Inspect unused sales invoices for consecutive prenumbering.

A client has a large and active investment portfolio that is kept in a bank safe deposit box. If the auditor is unable to count the securities at the balance sheet date, the auditor most likely will:

A. Request the bank to confirm to the auditor the contents of the safe deposit box at the balance sheet date.

B. Examine supporting evidence for transactions occurring during the year.

C. Count the securities at a subsequent date and confirm with the bank whether securities were added or removed since the balance sheet date.

D. Request the client to have the bank seal the safe deposit box until the auditor can count the securities at a subsequent date.

Which of the following statements is correct if there is an increase in the resources available within an economy?

A. More goods and services will be produced in the economy.

B. The economy will be capable of producing more goods and services.

C. The standard of living in the economy will rise.

D. The technological efficiency of the economy will improve.

Under monopolistic competition, strategic plans focus on:

A. Profitability from production levels that maximize profits.

B. Maintaining the market share and being responsive to market conditions related to sales price.

C. Maintaining the market share and planning for enhanced product differentiation.

D. Maintaining the market share, ensuring product differentiation, and adapting to price changes or required changes in production volume.

Strategic planning activities normally involve which of the following efforts:

I. Strategic Positioning.

II. Value Chain Analysis.

III.

Balance Scorecard Development.

A.

I.

B.

I and II.

C.

I and III.

D.

I, II, and III.

How should the effect of a change in accounting principle that is inseparable from the effect of a change in accounting estimate be reported?

A. As a component of income from continuing operations.

B. By restating the financial statements of all prior periods presented.

C. As a correction of an error.

D. By footnote disclosure only.

In 19X4, Smith, a divorced person, provided over one half the support for his widowed mother, Ruth, and his son, Clay, both of whom are U.S. citizens. During 19X4, Ruth did not live with Smith. She received $9,000 in Social Security benefits. Clay, a 25 year-old full-time graduate student, and his wife lived with Smith. Clay had no income but filed a joint return for 19X4, owing an additional $500 in taxes on his wife's income. How many exemptions was Smith entitled to claim on his 19X4 tax return?

A. 4

B. 3

C. 2

D. 1

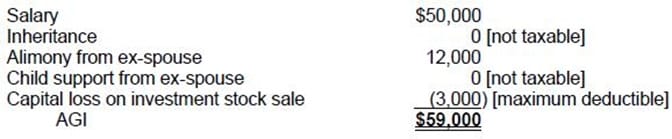

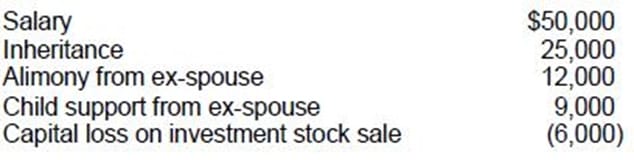

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000

B. $59,000

C. $62,000

D. $84,000