FINANCIAL-ACCOUNTING-AND-REPORTING Online Practice Questions and Answers

According to the FASB conceptual framework, the usefulness of providing information in financial statements is subject to the constraint of:

A. Consistency.

B. Cost-benefit.

C. Reliability.

D. Representational faithfulness.

How should the effect of a change in accounting principle that is inseparable from the effect of a change in accounting estimate be reported?

A. As a component of income from continuing operations.

B. By restating the financial statements of all prior periods presented.

C. As a correction of an error.

D. By footnote disclosure only.

On November 1, 20X2, Smith Co. contracted to dispose of an industry segment. Throughout 20X2 the segment had operating losses. These losses were expected to continue until the segment's disposition. If a loss is projected on final disposition, how much of the operating losses should be included in the loss from discontinued operations reported in Smith's 20X2 income statement?

I. Operating losses for the period January 1 to October 31, 20X2.

II. Operating losses for the period November 1 to December 31, 20X2.

III.

Estimated operating losses for the period January 1 to February 28, 20X3.

A.

II only.

B.

II and III only.

C.

I and III only.

D.

I and II only.

If a company is not presenting comparative financial statements, the correction of an error in the financial statements of a prior period should be reported, net of applicable income taxes, in the current:

A. Retained earnings statement after net income but before dividends.

B. Retained earnings statement as an adjustment of the opening balance.

C. Income statement after income from continuing operations and before extraordinary items.

D. Income statement after income from continuing operations and after extraordinary items.

The cumulative effect of a change in accounting estimate should be shown separately: A. On the income statement above income from continuing operations.

B. On the income statement after income from continuing operations and before extraordinary items.

C. On the retained earnings statement as an adjustment to the beginning balance.

D. It should not be recorded separately on any financial statement.

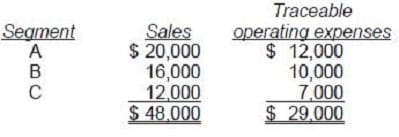

Taft Corp. discloses supplemental industry segment information. The following information is available for 1992: Additional 1992 expenses, not included above, are as follows:

Indirect operating expenses $7,200 General corporate expenses 4,800

Segment C's 1992 operating profit was:

A. $5,000

B. $3,200

C. $2,600

D. $2,000

In financial reporting of segment data, which of the following items is always used in determining a segment's operating income?

A. Income tax expense.

B. Sales to other segments.

C. General corporate expense.

D. Gain or loss on discontinued operations.

Which of the following factors determines whether an identified segment of an enterprise should be reported in the enterprise's financial statements under SFAS No. 131, Disclosures about Segments of an Enterprise and Related Information?

I. The segment's assets constitute more than 10% of the combined assets of all operating segments.

II.

The segment's liabilities constitute more than 10% of the combined liabilities of all operating segments.

A.

I only.

B.

II only.

C.

Both I and II.

D.

Neither I nor II.

Which of the following types of entities are required to report on business segments?

A. Nonpublic business enterprises.

B. Publicly-traded enterprises.

C. Not-for-profit enterprises.

D. Joint ventures.

Which of the following statements regarding fair value is/are correct?

I. The fair value of an asset or liability is specific to the entity making the fair value measurement.

II. Fair value is the price to acquire an asset or assume a liability.

III. Fair value includes transportation costs, but not transaction costs.

IV.

The price in the principal market for an asset or liability will be the fair value measurement.

A.

I and II

B.

I and IV

C.

II and III

D.

III and IV